What $100 Oil Means for Your Formula

A postscript to our series on the forces reshaping polymer choices in beauty formulations

On February 28, oil was $70 a barrel. Two weeks later it crossed $100. The Strait of Hormuz, a place most of us couldn’t find on a map a few months ago, effectively shut down overnight, taking ~10m barrels of oil and 20% of the world’s natural gas out of global markets.

Over the past week, we’ve seen global energy markets in turmoil, the IEA releasing 400 million barrels from strategic reserves, and several Asian petrochemical manufacturers declaring force majeure as they cancel runs at their refineries.

If you run a beauty brand, it’s no secret that everything from your ingredients to your packaging to the energy that runs your contract manufacturer’s facility can likely be traced back to barrels of crude oil. But how will it affect your bottom line, if at all? We decided to crunch some numbers and try to find out.

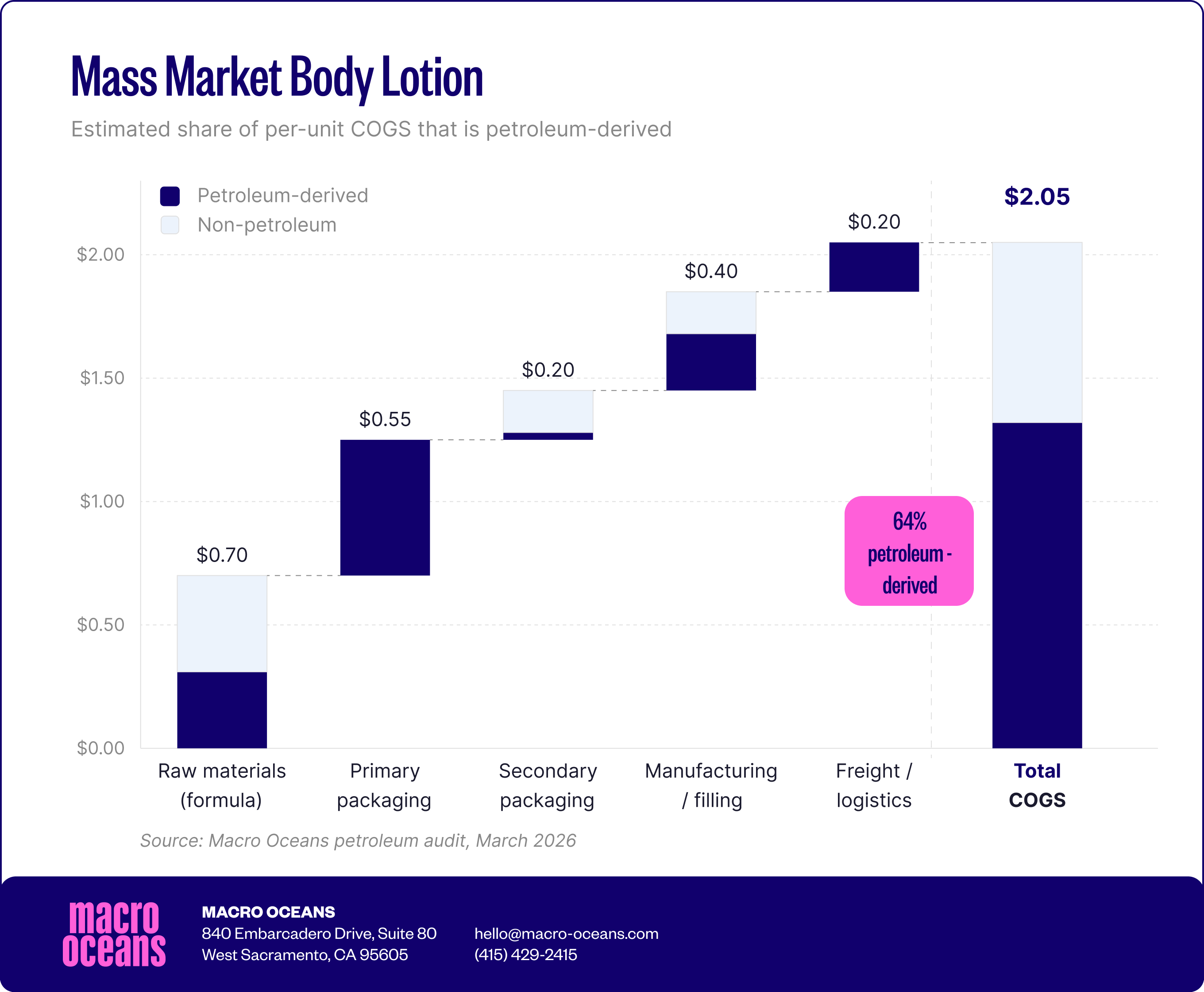

The Petroleum Audit

We took a standard mass-market body lotion, the kind you’d find on any drugstore shelf for under $10, and tagged every input that is derived from, or dependent on, petroleum. This includes not just the obvious ones like petrolatum and mineral oil, but the less visible dependencies such as silicones synthesized through petroleum intermediates, synthetic polymers built from petroleum-derived monomers, PEG emulsifiers, synthetic fragrance compounds, and the preservative systems that rely on petrochemical feedstocks.

Then we looked beyond the formula. First up: packaging. Nearly all these mass-market lotions are in HDPE bottles (petroleum-derived), have polypropylene caps and pumps (petroleum-derived) and adhesive labels (petroleum-derived). Finally, we added in the fossil fuel energy powering the contract manufacturing line (~57% of the US grid is still fossil fuel) and the diesel fuel that moves the finished product from factory to warehouse to store.

Here’s what we found.

Inside the formula: approximately 14% of the formula by weight is directly petroleum-derived (petrolatum, silicones, synthetic fragrance, synthetic emulsifiers). When you include ingredients where one part of the molecule is synthesized from petroleum feedstocks, that number grows to roughly 27% of the formula by weight. In cost terms, about 40–45% of raw material spend traces back to petroleum-derived chemistry.

Packaging: the primary container—bottle, cap, pump—is 100% petroleum-derived plastic. This is often the single largest petroleum-exposed cost component per unit, sometimes larger than all the petroleum-derived ingredients combined.

Manufacturing and freight: with the US grid running roughly 57% fossil fuel and freight moving almost entirely on diesel, these add another layer of petroleum exposure to every unit produced and shipped.

When you add it all up, roughly two-thirds of the total cost to produce and ship one unit of a typical mass-market body lotion is built on petroleum-derived inputs.

What this means for your COGS

An important caveat: exposure does not equal price sensitivity. A 50% oil spike will not produce a 32% increase in your COGS overnight.

The real-world chain from crude oil to cosmetic ingredient is long and has many buffers. Ingredient suppliers may be locked into long-term contracts, manufacturers may absorb margin hits rather than raise prices to brand customers. The price transmission mechanism is slow and uneven.

But if two-thirds of your cost structure sits on a petroleum foundation, then you should expect the oil price shock to ripple through to your bottom line eventually. Short disruptions get buffered. Long ones don’t.

Long Global Supply Chains are Inherently Fragile

This is the fourth major supply chain shock in five years. COVID shut down factories and stretched ingredient lead times from weeks to months. The Suez Canal blockage halted $9 billion in daily trade. The Russia-Ukraine conflict tripled European gas prices and rippled through chemical manufacturing for a year. Tariffs have reshuffled cross-border sourcing with the rules still changing. And now the Strait of Hormuz - a global gateway for oil and gas - is effectively closed, with Brent crude up over 50% in weeks.

Each of these events was unpredictable in its specifics. But the pattern is entirely predictable: if your supply chain is built on petroleum-derived inputs, logistics, and packaging, you are structurally exposed to geopolitical, environmental, and economic shocks that you cannot foresee or control. What alternatives do you have?

What Resilience Looks Like

Today there are many ingredients, materials, and sourcing strategies that can reduce your petroleum dependency. Think of this not as a sustainability exercise (though it is climate positive too), but as a supply chain resilience plan.

Bio-based raw materials: from vegetable glycerin, to fermentation-derived ingredients like bio-based surfactants, and next generation all natural rheology modifiers (plug: have you heard about Big Kelp Flex, our seaweed-derived cellulose biopolymer?), there are lots of options reaching performance parity with synthetic materials that have dominated formulations for decades. We mapped this landscape in detail in our recent series on natural polymer alternatives.

Domestic and regenerative sourcing: Ingredients grown domestically—kelp from US waters, oats from US farms, botanicals from traceable supply chains—don’t transit the Strait of Hormuz or require oil or gas as a feedstock. Regenerative crops like kelp, grow with limited inputs: no land, no freshwater, no fertilizers, no pesticides. These new supply chains are traceable, on-shore, and insulated from the geopolitical risks.

Packaging alternatives: PCR (post-consumer recycled) plastics, bio-based polyethylene, aluminum, glass, and refillable systems all reduce petroleum packaging exposure. Each has trade-offs, but the options are more viable at scale today than even a few years ago.

Energy and freight: The US grid is evolving. In California, 66% of the grid is now powered by clean energy. Nationwide, solar now accounts for half of all new generating capacity. Manufacturers with renewable energy contracts are already partially insulated from fossil fuel volatility. Freight remains petroleum-dependent for now, a weak point in all supply chains.

A (Beautiful) Silver Lining

Every supply chain shock divides the beauty industry into two groups: those scrambling to manage the fallout, and those who already made the structural changes that insulate them from it. The brands that have reformulated away from petroleum-derived polymers or switched bio-based packaging are unlikely to be in emergency calls debugging their supply chains.

Here’s a useful mental model when tackling this issue. Think of petroleum dependency like technical debt in software: it accumulates quietly, doesn’t cause problems most of the time, and then one day the system breaks under stress and you discover exactly how much you’ve been borrowing against the future. Inertia is hard to overcome; diversifying ingredient sourcing, exploring bio-based materials, all takes time, effort and investment. But if you don’t do it, then you’re adding to that debt and the principal payments come due when the next crisis hits.

The beauty industry has spent the last decade asking: how do we make our products cleaner? The Covid pandemic and this oil shock is forcing us to reckon with a harder, more consequential question: how do we make our supply chains resilient?

The good news is that the answers are increasingly the same. Bio-based, domestically sourced, regenerative ingredients don’t just satisfy consumers and regulators. They also don’t depend on a 21-mile-wide strait staying open.